Thailand regional operating headquarters in 2026

- The Regional Operating Headquarters (ROH) in Thailand is a business entity that provides its foreign branches and associated enterprises i) managerial and administrative services ii) technical services and iii) other supporting services;

- For our Client’s existing company in Thailand to become ROH, our Client must notify the Revenue Department by submitting the notification form;

- For a Thai company subject to Foreign Business Act (FBA) 1999 and wants to change its structure to ROH:

- The company must first get approval from the Department of Commercial Registration to amend its business scope and ensure it covers the activities of ROH;

- Approval usually takes approximately 60 days to be granted;

- After the approval, the company can commence its operations as ROH.

- ROH which has been granted investment promotion privileges may employ expatriates. These expatriates can work only in the positions approved by the Foreign Experts Services Unit;

- For ROH that does not have promotion investment privileges, the ROH must apply for i) work permit at the One Stop Service Center for Visa and Work Permit and ii) apply for visa at the Immigration Bureau.

-

ROH criteria

Below are the qualifying criteria to receive tax benefits as an ROH:

- THB$10 Million or more for paid-up capital at the end of each accounting period;

- Qualified services provided to branches or associated enterprises in at least 3 countries;

- To notify the Revenue Department about the incorporation as ROH. Benefits will be given once the accounting period has been notified;

- At least half of the ROH’s total income is derived from i) administrative, ii) technical and iii) other supporting services to its branches or associated enterprises in other countries and royalties received outside Thailand for the use of ROH’s R&D;

- Total business spending in Thailand of at least THB$15 million per year or investment spending of at least THB$30 million per year paid in Thailand;

- Foreign associated enterprises must have actual business operations including i) management staff and ii) employees.

On a case-by-case basis

- The last criteria can be mitigated to one-third of the total income in the first three accounting periods of its operation as ROH;

- In the case of force majeure, the Director-General of the Revenue Department may lower the income threshold for one accounting period, subject to approval.

-

Advantages of ROH

- Reduced corporate tax rate at 10% on:

- Income derived from services to the ROH’s foreign subsidiaries;

- Royalties derived from the ROH’s foreign branches and associated enterprises for Research and Development (R&D) done in Thailand;

- Royalties received from a third party providing services to the ROH’s subsidiaries using the ROH’s own R&D technology;

- Net profits and interest received from ROH’s foreign subsidiaries for loans granted, if the loans are from third-party sources.

- Withholding tax exemption for:

- Dividends received by ROH from foreign affiliates;

- Dividends paid out of the ROH’s qualified income to foreign shareholders not conducting business in Thailand.

- Accelerated depreciation rate of 25% for buildings on the date of acquisition. The residual value can be depreciated within 20 years.

- Reduced corporate tax rate at 10% on:

-

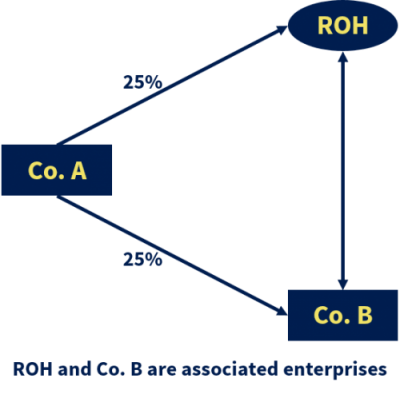

Associated enterprises of ROH

A company is considered as an ROH’s associated enterprise based on the following 2 criteria:

A company is considered as an ROH’s associated enterprise based on the following 2 criteria:Shareholding

- ROH holds at least 25% of the associated enterprise’s issued capital or;

- The company holds at least 25% of ROH’s issued capital or;

- The company holds at least 25% of ROH and other company’s issued capital. In this case, ROH and the other company are both regarded as associated enterprises.

Control

- The ROH has control over the company or;

- The associated enterprise has control over the ROH or;

- The associated enterprise has control over the ROH and other company, where both the ROH and the other company are regarded as associated enterprises.

-

Qualifying services eligible for tax privileges

Qualifying services for tax privileges that ROH provides to its branches or associated enterprises are i) Managerial and administrative ii) technical services and iii) supporting services. Some of the supporting services include:

- General administration and business planning;

- Procurement of raw materials and components;

- Research and development;

- Marketing and sales promotion planning;

- Financial advisory services;

- Economic and investment research.

-

Foreign companies in Thailand and ROH non-tax privileges

- For a foreign-owned company in Thailand to benefit from non-tax privileges given under Promotion Investment Act, they must first apply for investment promotion privileges from the Board of Investment (BOI). Thereafter, notify the Revenue Department of their intention to become ROH;

- Non-tax privileges that will be granted include:

- Land ownership;

- Majority or total foreign ownership;

- Hiring of expatriates;

- Repatriation of foreign currency.

-

ROH tax considerations

- Only qualified income and expenses will be taxable under the ROH scheme;

- The ROH must file Corporate Income Tax using i) P.N.D. 50 Form for annual filing and ii) P.N.D. 51 Form for the half-yearly filing;

- If ROH has other income that is subject to the normal corporate tax rate of 30% or other rates granted by BOI, the ROH must file 2 returns using each form:

- 1st return – for income that has been granted reduction/exemption under ROH scheme;

- 2nd return – for income that is subject to normal tax rate of 30% or special rates granted by BOI.

- Expatriates working for ROH are subject to a reduced tax rate of 15% on their gross income up to their first 4 years of employment. Thereafter, he will be subject to standard personal income tax rates;

- For expatriates sent to work abroad by the ROH, they will receive tax exemption in Thailand under the following conditions:

- Their income is paid by the foreign company and;

- The income is not part of the ROH nor its associated enterprise’s expenses in Thailand.

A company is considered as an ROH’s associated enterprise based on the following 2 criteria:

A company is considered as an ROH’s associated enterprise based on the following 2 criteria:To compare different company formation options and understand how they differ in practice, see our company entities comparison in Thailand.